Back

BackLecture 11: Money & The Federal Reserve

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Lecture 11 - Money & The Federal Reserve (Post- Lecture):

What is Money?

Money is any generally accepted means of payment used to buy goods and services. It is broader than just currency (paper bills and coins), as it includes other forms of payment such as bank deposits and digital transfers.

Currency: Physical bills and coins used in transactions.

Money: Any generally accepted means of payment, including currency, checkable deposits, and transfer payments

Functions of Money

Money serves three primary functions in an economy:

Medium of Exchange: Used to trade for goods and services, eliminating the inefficiency of barter systems = require a double coincidence of wants. (Two parties wanting something different from one another)

Unit of Account: Provides a common measure for valuing goods and services, simplifying price comparisons and record-keeping. (e.g., every expense in the USA is measured through USD.)

Store of Value: Allows individuals to transfer purchasing power from the present to the future, though its importance has declined with the rise of alternative assets.

Types of Money

Commodity Money: Actual goods used as money (e.g., gold, silver, tobacco) that have multiple purposes, "intrinsic value" [gold can also be jewelry, tobacco can be used to smoke cigarettes].

Commodity-Backed Money: Certificates or notes that can be exchanged for a fixed quantity of a commodity. (e.g., gold certificates)

Bitcoin tried to mimic commodity-backed money.

Fiat Money: Money with no intrinsic value (NOT multi-purpose), established as money by government decree (e.g., modern U.S. dollar).

PROBLEM WITH FIAT MONEY;

Examples and Applications

In colonial Virginia, tobacco was used as money.

In modern prisons, items like cigarettes or cans of mackerel have served as money due to their acceptability and stable value.

Measuring the Money Supply

Definitions and Components

The money supply in an economy is measured by aggregating various forms of money. The two main measures are:

M1: Includes currency, checkable deposits, and savings deposits (since 2020), as well as traveler’s checks.

M2: Includes everything in M1 plus money market mutual funds and small-denomination time deposits (certificates of deposit). (Look at canvas slide definitions for these two).

Formula:

Credit cards are not included in the money supply, as they represent borrowed funds rather than actual money.

Cryptocurrency as Money

Cryptocurrencies like Bitcoin and Dogecoin can serve as a medium of exchange, though they are not issued by governments and their value is highly volatile. Their value is determined by supply and demand, and they are often used as speculative investments.

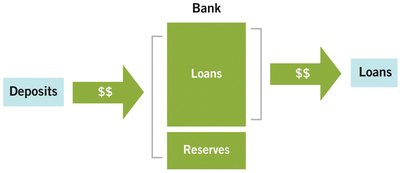

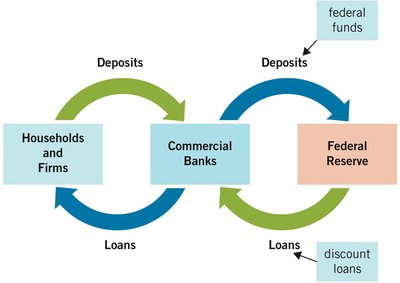

The Business of Banking and Money Creation (Commercial Banks):

Role of Banks in the Economy

Loans = primary USE of bank funds

Deposits = Primary SOURCE of bank funds Recall these definitions when looking at balance sheet.

Reserves: Bank deposits set aside; NOT lent out.

Banks are essential financial intermediaries. They accept deposits and extend loans, playing a critical role in the market for loanable funds and in determining the money supply.

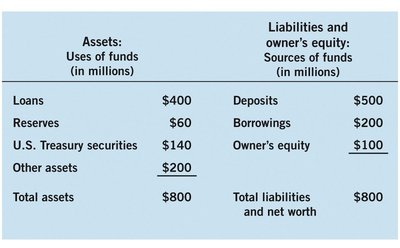

Bank Balance Sheets

A bank’s balance sheet summarizes its financial position, listing assets (loans, reserves, securities) and liabilities (deposits, borrowings, owner’s equity).

Assets: Uses of funds (in millions) | Liabilities and owner's equity: Sources of funds (in millions) |

|---|---|

Loans $400 | Deposits $500 |

Reserves $60 | Borrowings $200 |

U.S. Treasury securities $140 | Owner’s equity $100 |

Other assets $200 | |

Total assets $800 | Total liabilities and net worth $800 |

Fractional Reserve Banking

Modern banks operate under a fractional reserve system, holding only a fraction of deposits as reserves and lending out the rest. This system allows banks to create money through the lending process.

Bank Runs and the FDIC

Bank runs occur when many depositors withdraw funds simultaneously, fearing the bank’s insolvency. The FDIC insures deposits up to $250,000, reducing the risk of bank runs but introducing moral hazard, as banks and depositors may take on more risk knowing they are protected.

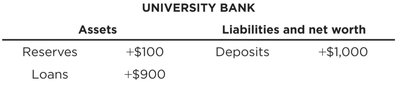

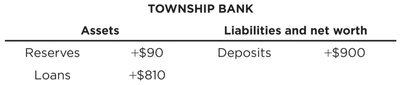

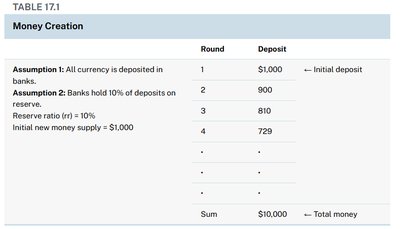

How Banks Create Money

The Money Multiplier Process

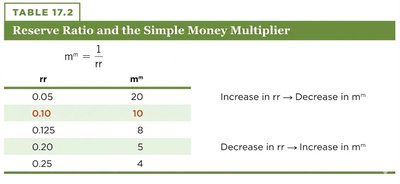

When banks receive deposits, they keep a fraction as reserves and lend out the rest. The process of lending and redepositing creates new money in the economy. The maximum potential increase in the money supply is determined by the simple money multiplier:

Simple Money Multiplier Formula: where rr is the required reserve ratio.

Round | Deposit |

|---|---|

1 | $1,000 |

2 | 900 |

3 | 810 |

4 | 729 |

... | ... |

Sum | $10,000 |

Why are banks important (reference Lecture 11 Review).

Limitations of the Money Multiplier

The simple money multiplier represents the maximum possible expansion of the money supply.

In reality, people hold some cash and banks may keep excess reserves, reducing the actual multiplier effect.

The process also works in reverse: withdrawals contract the money supply by a multiple of the withdrawal amount.

The Federal Reserve and Control of the Money Supply

Structure and Functions of the Federal Reserve

The Federal Reserve (the Fed) is the central bank of the United States, established in 1913. Its main responsibilities are:

Monetary Policy: Regulating the money supply to offset macroeconomic fluctuations.

Central Banking: Serving as a bank for commercial banks, holding their deposits and extending loans.

Bank Regulation: Ensuring the financial stability of banks and setting reserve requirements.

Monetary Policy Tools

The Fed uses several tools to manage the money supply and influence interest rates:

Interest on Reserve Balances (IORB): The Fed pays interest on reserves held by banks. Raising IORB encourages banks to hold more reserves and lend less, reducing the money supply. Lowering IORB has the opposite effect.

Overnight Reserve Repurchase Agreements (Reverse Repo): The Fed borrows cash overnight from financial institutions, temporarily pulling money out of the system to maintain target interest rates.

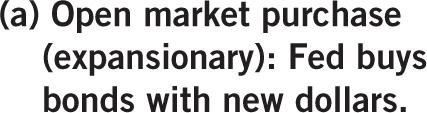

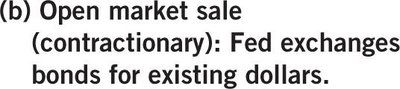

Open Market Operations: The Fed buys or sells government securities to increase or decrease the money supply. Buying securities injects money; selling securities withdraws money.

Quantitative Easing: The Fed purchases longer-term securities to target specific markets, used during extraordinary economic conditions.

Lending Facilities (Discount Window): The Fed extends loans to banks and, in special cases, to other institutions to maintain financial stability.

Summary Table: Monetary Policy Tools

Tool | Purpose | Effect on Money Supply |

|---|---|---|

Interest on Reserve Balances (IORB) | Influence bank lending | Increase (lower IORB) or decrease (raise IORB) |

Open Market Operations | Buy/sell securities | Increase (buy) or decrease (sell) |

Discount Window | Lend to banks | Increase (more lending) |

Quantitative Easing | Targeted asset purchases | Increase |

Reverse Repo | Short-term rate management | Decrease (temporarily) |

Conclusion

Money is a fundamental component of the macroeconomy, serving as a medium of exchange, unit of account, and store of value. Banks play a crucial role in creating money through fractional reserve banking, while the Federal Reserve manages the money supply using a variety of policy tools. Understanding these mechanisms is essential for analyzing macroeconomic policy and its effects on the broader economy.