Back

BackMoney, the Price Level, and Inflation: Study Notes for Macroeconomics

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Money, the Price Level, and Inflation

Introduction

This chapter explores the nature and functions of money, the structure and role of depository institutions and the central bank, the process of money creation, and the relationship between money, the price level, and inflation. Understanding these concepts is essential for analyzing monetary policy and its effects on the economy.

What is Money?

Definition and Functions of Money

Money is any commodity or token that is generally accepted as a means of payment.

It serves as a medium of exchange, unit of account, and store of value.

A means of payment is a method of settling a debt.

Medium of Exchange

A medium of exchange is an object accepted in exchange for goods and services.

Without money, exchange would require barter, which is inefficient due to the need for a double coincidence of wants.

Unit of Account

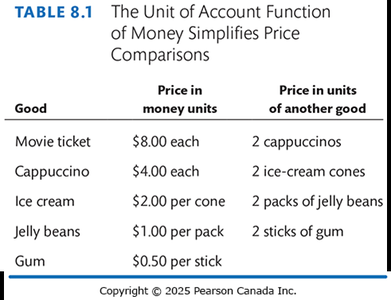

A unit of account is an agreed measure for stating prices, simplifying price comparisons.

Example: Table 8.1 shows how money allows for easy comparison of prices across different goods.

Store of Value

Money can be held and used for future purchases, maintaining value over time (though inflation can erode this).

Money in Canada Today

Money consists of currency (notes and coins) and deposits at banks and other depository institutions.

Deposits can be chequable (allowing payments by cheque or e-transfer) or non-chequable (interest-bearing, not directly transferable).

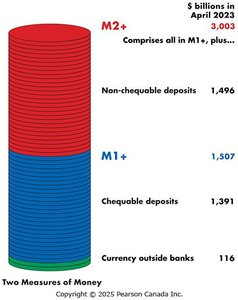

Measures of Money: M1+ and M2+

M1+: Currency outside banks + chequable deposits.

M2+: M1+ plus non-chequable deposits.

Example: In April 2023, M1+ was $1,507 billion and M2+ was $3,003 billion.

What is Not Money?

Credit cards, debit cards, and money wallets are not money; they are payment mechanisms.

Cheques and e-transfers are instructions to transfer money, not money themselves.

Depository Institutions

Types of Depository Institutions

Chartered banks: Private firms chartered under the Bank Act to receive deposits and make loans.

Credit unions and caisses populaires: Cooperative organizations for members, regulated under specific acts.

Trust and mortgage loan companies: Specialized in trust and mortgage services.

Functions and Asset Management

Depository institutions aim to maximize owners' wealth by lending at higher rates than they pay on deposits.

They balance profit and prudence, ensuring depositors can access funds.

Assets include reserves, liquid assets, securities, and loans.

Sources and Uses of Funds

Sources: Deposits, borrowing, own capital.

Uses: Reserves, liquid assets, securities, loans.

Source/Use | Amount ($ billions) | Percentage of Deposits |

|---|---|---|

Total funds | 3,983 | 143.6 |

Deposits | 2,773 | 100.0 |

Borrowing | 722 | 26.0 |

Own capital | 488 | 17.6 |

Reserves | 227 | 8.1 |

Liquid assets | 129 | 4.7 |

Securities | 507 | 18.3 |

Loans | 3,120 | 112.5 |

Economic Benefits of Depository Institutions

Create liquidity

Pool risk

Lower the cost of borrowing

Lower the cost of monitoring borrowers

Regulation: Insolvency and Illiquidity

Insolvency: Occurs if liabilities exceed assets; banks must maintain a capital buffer.

Illiquidity: Occurs if a bank cannot meet withdrawal demands; the Bank of Canada provides reserves to prevent this.

Financial Innovation

Financial innovation aims to lower deposit costs or increase lending returns, changing the composition of money over time.

The Bank of Canada

Role and Structure

The Bank of Canada is the central bank, regulating depository institutions and controlling the money supply.

Functions: Banker to banks and government, lender of last resort, sole issuer of bank notes.

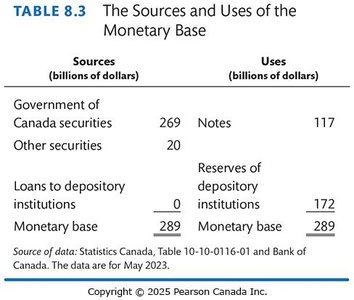

Balance Sheet and Monetary Base

Assets: Government securities, loans to depository institutions.

Liabilities: Bank notes, depository institution deposits.

The monetary base is the sum of Bank of Canada notes, coins, and depository institution deposits at the Bank of Canada.

Sources (billions of dollars) | Uses (billions of dollars) |

|---|---|

Government of Canada securities: 269 | Notes: 117 |

Other securities: 20 | Reserves of depository institutions: 172 |

Loans to depository institutions: 0 | Monetary base: 289 |

Monetary base: 289 |

Policy Tools

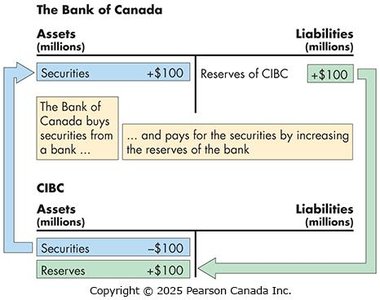

Open market operations: Buying or selling government securities to influence bank reserves.

Bank rate: The interest rate charged on short-term loans to major depository institutions, anchoring other short-term rates.

Open Market Operations: Effects

Purchasing securities increases bank reserves; selling securities decreases reserves.

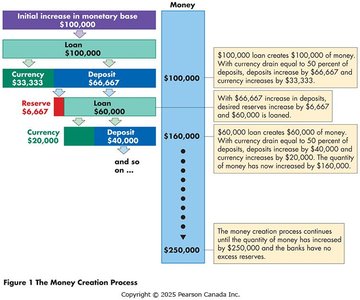

How Banks Create Money

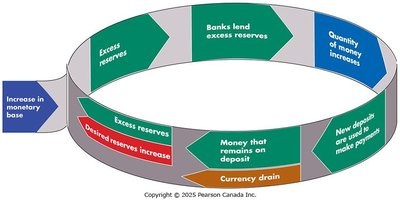

Money Creation Process

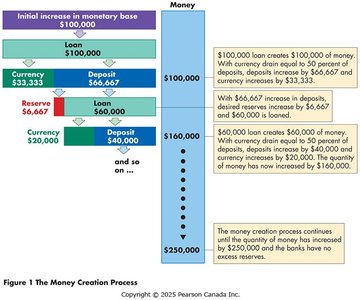

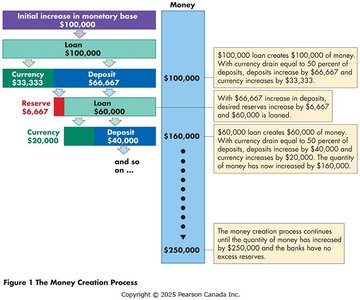

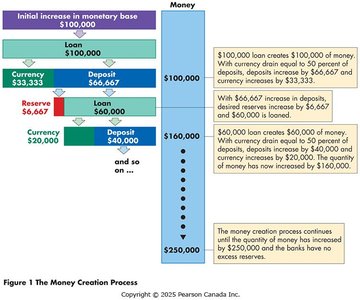

Banks create deposits (money) by making loans, limited by the monetary base, desired reserves, and desired currency holding.

Desired reserve ratio: The fraction of deposits banks plan to hold as reserves.

Currency drain ratio: The fraction of money people wish to hold as currency.

The Money Multiplier

The money multiplier is the ratio of the change in the quantity of money to the change in the monetary base.

Formula:

The multiplier depends on the desired reserve ratio and the currency drain ratio; the smaller these ratios, the larger the multiplier.

The Money Market

Determinants of Money Holding

The quantity of money people plan to hold depends on the price level, nominal interest rate, real GDP, and financial innovation.

Nominal money: Measured in dollars; real money: Nominal money divided by the price level.

Formula:

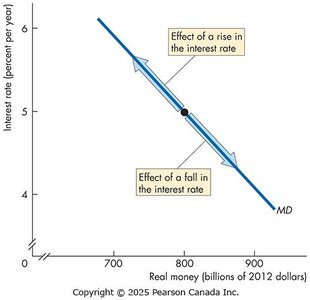

Demand for Money

The demand for money is the relationship between the quantity of real money demanded and the nominal interest rate, holding other factors constant.

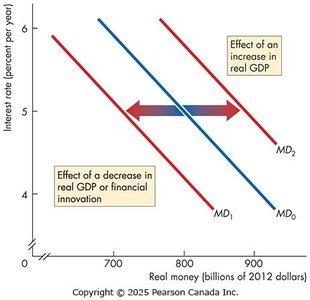

Shifts in the Demand for Money

Increases in real GDP shift the demand curve right; decreases in real GDP or financial innovation shift it left.

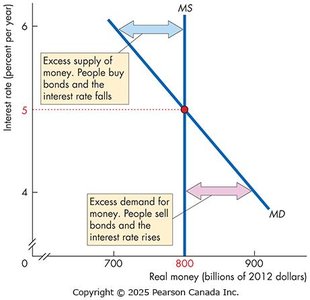

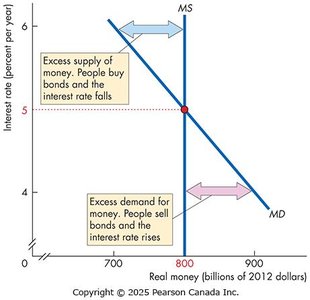

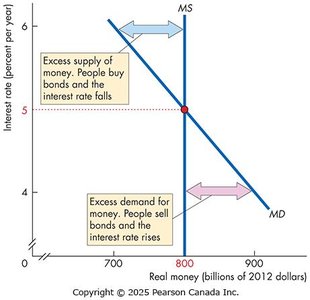

Money Market Equilibrium

Equilibrium occurs when the quantity of money demanded equals the quantity supplied.

Short-run: The Bank of Canada adjusts the money supply to target a specific interest rate.

Adjustments in the Money Market

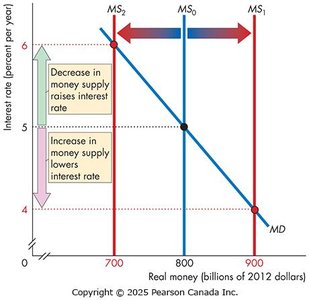

If the interest rate is above equilibrium, excess supply of money leads people to buy bonds, lowering the interest rate.

If the interest rate is below equilibrium, excess demand for money leads people to sell bonds, raising the interest rate.

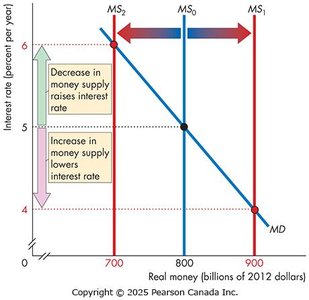

Short-Run Effects of Money Supply Changes

Increasing the money supply lowers the interest rate; decreasing it raises the interest rate.

Long-Run Equilibrium

In the long run, the loanable funds market determines the real interest rate, and the price level adjusts to equate real money supply and demand.

Increases in the money supply lead to proportional increases in the price level, with no real effects on GDP or employment.

Money, the Price Level, and Real GDP

The Quantity Theory of Money

The quantity theory of money states that, in the long run, an increase in the quantity of money brings an equal percentage increase in the price level.

Based on the velocity of circulation (V) and the equation of exchange:

If M does not influence V or Y, then changes in M cause proportional changes in P.

Expressed in growth rates:

Rearranged:

If velocity is constant, inflation equals money growth minus real GDP growth.

Mathematical Note: The Money Multiplier

Example Calculation

Suppose the desired reserve ratio is 10% and the currency drain ratio is 50%.

An increase in the monetary base by $100,000 leads to a total increase in money of $250,000.

The money multiplier formula is:

Where C/D is the currency drain ratio and R/D is the desired reserve ratio.

In the example, C/D = 0.5, R/D = 0.1, so: