Back

BackShort-Run Fluctuations and Business Cycles: Macroeconomic Study Guide

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Short-Run Fluctuations (Business Cycles)

Introduction to Economic Fluctuations

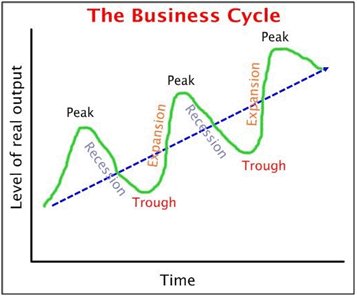

Economic fluctuations, also known as business cycles, refer to short-run changes in the growth of Gross Domestic Product (GDP). These cycles are characterized by alternating periods of economic expansion and recession. Economists analyze business cycles by comparing the path of real GDP to a long-term trend line.

Recession: A period of negative economic growth lasting at least two quarters.

Expansion: A period of positive growth, occurring between recessions.

Peak: The highest point before a recession begins.

Trough: The lowest point before an expansion begins.

Key Properties of Economic Fluctuations

Economic fluctuations exhibit three main properties:

Co-movement: Many macroeconomic variables move together during booms and busts. For example, real consumption, real investment, and employment are pro-cyclical (move with GDP), while unemployment is counter-cyclical (moves opposite to GDP).

Limited Predictability: The timing of recessions and expansions is difficult to forecast. There is no repetitive, easily predictable pattern.

Persistence: Economic growth or contraction tends to persist from one quarter to the next.

Historical Business Cycles

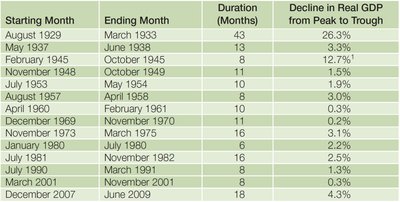

Since 1929, recessions have occurred about once every six years, typically lasting about one year.

Starting Month | Ending Month | Duration (Months) | Decline in Real GDP from Peak to Trough |

|---|---|---|---|

August 1929 | March 1933 | 43 | 26.3% |

May 1937 | June 1938 | 13 | 6.3% |

February 1945 | October 1945 | 8 | 12.7% |

November 1948 | October 1949 | 11 | 1.5% |

July 1953 | May 1954 | 10 | 2.6% |

August 1957 | April 1958 | 8 | 3.0% |

April 1960 | February 1961 | 10 | 0.3% |

December 1969 | November 1970 | 11 | 0.6% |

November 1973 | March 1975 | 16 | 3.1% |

January 1980 | July 1980 | 6 | 2.2% |

July 1981 | November 1982 | 16 | 2.6% |

July 1990 | March 1991 | 8 | 1.3% |

March 2001 | November 2001 | 8 | 0.3% |

December 2007 | June 2009 | 18 | 4.3% |

Macroeconomic Equilibrium and Economic Fluctuations

Causes of Economic Fluctuations

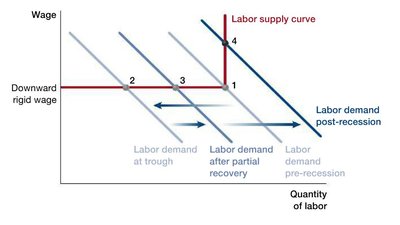

Economic fluctuations are often triggered by unexpected shifts in labor demand, known as shocks. At the onset of a recession, the labor demand curve shifts left due to:

A fall in output prices

A decrease in output demand

A decrease in labor productivity

A rise in other input prices

Labor Market Dynamics During Recession

A leftward shift in labor demand typically results in no change in the wage rate (due to downward wage rigidity) but a decrease in the quantity of labor, leading to a reduction in real GDP.

Okun's Law

Okun's Law describes the relationship between changes in the unemployment rate and the growth rate of real GDP:

Formula: where is the annual growth rate of real GDP.

Schools of Thought on Economic Fluctuations

Real Business Cycle Theory: Emphasizes changes in productivity and technology. Supply shocks (e.g., technological advances or increases in input prices) drive cycles. Market mechanisms dominate, with little role for government intervention.

Keynesian Theory: Focuses on business and consumer expectations ("animal spirits"). Changes in sentiment affect consumption and investment. Recessions are caused by low demand; expansions by increased spending. Government policy can alter the business cycle.

Financial and Monetary Theory: (Milton Friedman) Looks at changes in prices and interest rates. A decrease in money supply (M2) lowers price levels and increases real interest rates, reducing employment and investment.

Multipliers and Downward Wage Rigidity

Multipliers: Amplify the effects of economic shocks. For example, a negative consumption shock reduces household income, further shifting labor demand left and deepening the recession.

Downward Wage Rigidity: Wages do not easily decrease, leading to greater reductions in employment during recessions.

Recovery from Recession

Economic recovery can occur through:

Market Forces: Inventory rebuilding, renewed household spending, healthier firms purchasing bankrupt firms, technological advances, and financial intermediation.

Government Policies: Expansionary monetary policy (lowering interest rates, raising inflation) and fiscal policy (increasing government spending or lowering taxes).

Modeling Expansions

Expectations and Labor Demand

During expansions, optimistic expectations by firms (e.g., technology companies anticipating higher demand) lead to increased labor demand, shifting the labor demand curve to the right.

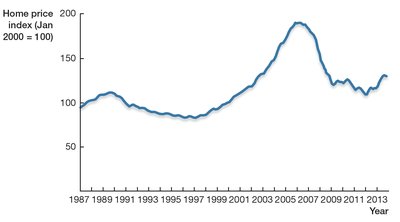

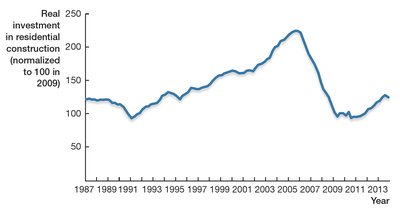

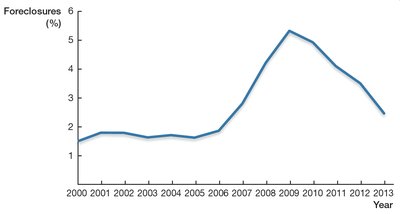

The Great Recession of 2007–2009

Causes of the 2007–2009 Recession

The recession was driven by several factors:

Monetary policy kept interest rates low, fueling a housing bubble.

Financial firms engaged in irresponsible lending to subprime borrowers.

Consumers took on loans they could not afford.

Mortgage-backed securities risks were underestimated.

Bank runs occurred in the "shadow banking system."

Key Factors in the Crisis

Collapse in Housing Prices: Led to a sharp decline in new construction.

Sharp Drop in Consumption: Households reduced spending, deepening the recession.

Spiraling Mortgage Defaults: Many banks failed, causing the financial system to freeze.

Summary of Key Ideas

Recessions: Periods (lasting at least two quarters) in which real GDP falls.

Three Features of Fluctuations: Co-movement, limited predictability, and persistence.

Sources of Fluctuations: Technology shocks, changing sentiments, and monetary/financial factors.

Amplification: Economic shocks are amplified by downward wage rigidity and multipliers.

Economic Booms: Periods of GDP expansion, increasing employment and declining unemployment.

2007–2009 Recession: Driven by a collapsing housing bubble, fall in household wealth, and a financial crisis.