Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Bank Reconciliation definitions

You can tap to flip the card.

Bank Reconciliation

You can tap to flip the card.

👆

Bank Reconciliation

Process of comparing a company's records with the bank statement to identify and adjust for timing differences and errors.

Track progress

Control buttons has been changed to "navigation" mode.

1/14

Related flashcards

Related practice

Recommended videos

Bank Reconciliation quiz #1

Bank Reconciliation

40 Terms

Bank Reconciliation quiz #2

Bank Reconciliation

40 Terms

Bank Reconciliation quiz #3

Bank Reconciliation

19 Terms

Bank Reconciliation

6. Internal Controls and Reporting Cash

10 problems

Topic

Journal Entries for Bank Reconciliation

6. Internal Controls and Reporting Cash

7 problems

Topic

6. Internal Controls and Reporting Cash

8 topics

15 problems

Chapter

Guided course

04:57

Bank Reconciliation:Bank Column

3329

views

98

rank

Guided course

05:15

Bank Reconciliation:Book Column

2279

views

68

rank

Terms in this set (14)

Hide definitions

Bank Reconciliation

Process of comparing a company's records with the bank statement to identify and adjust for timing differences and errors.

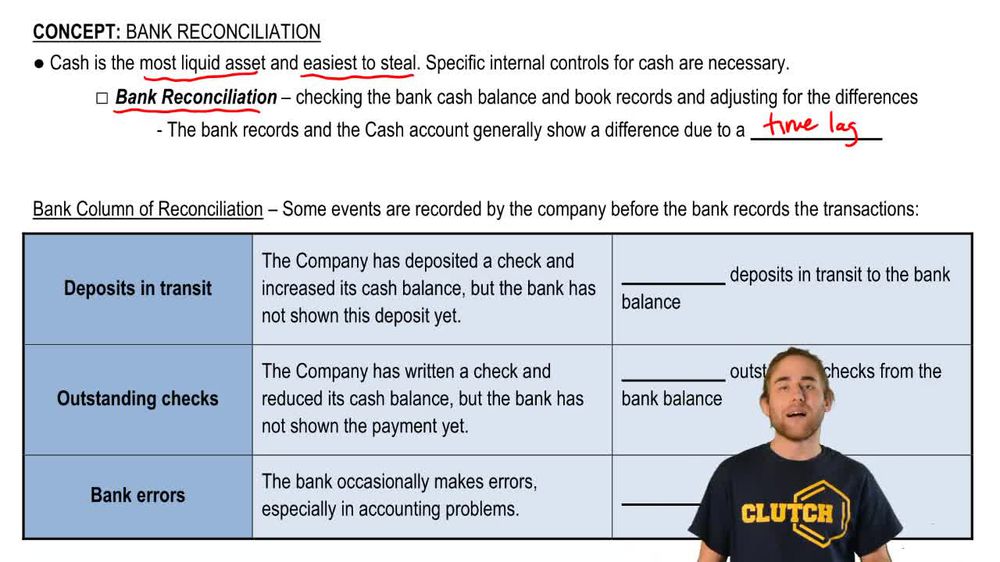

Deposits in Transit

Cash receipts recorded by the company but not yet processed or cleared by the bank at the statement date.

Outstanding Checks

Checks issued and recorded by the company but not yet cleared or deducted by the bank.

Bank Errors

Mistakes made by the bank in recording transactions, requiring correction to reflect the accurate account balance.

Book Errors

Mistakes in the company's accounting records that must be identified and corrected during reconciliation.

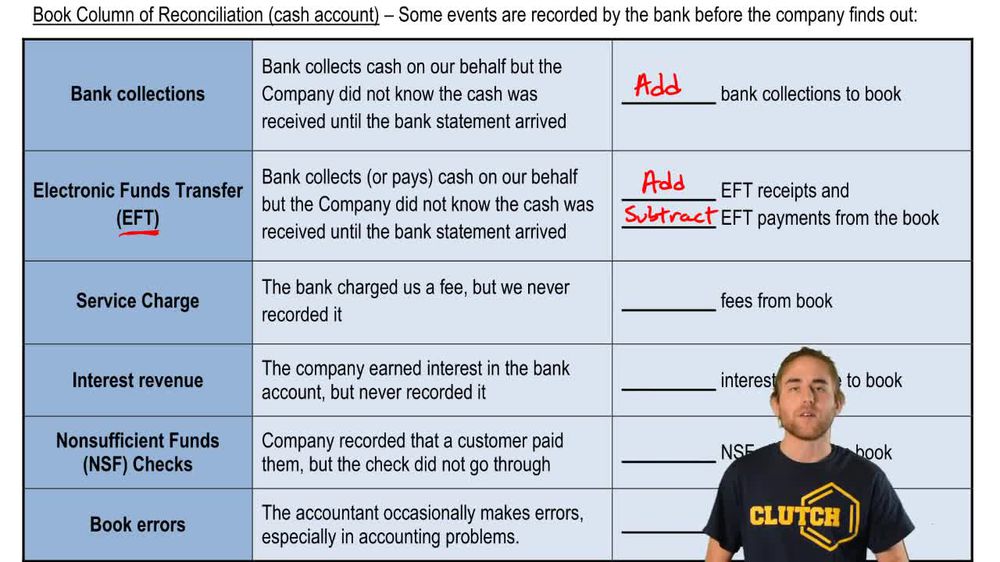

Bank Collections

Funds collected by the bank on behalf of the company, often without prior notice, increasing the book balance.

Electronic Funds Transfer

Automatic movement of money into or out of the company's account, such as direct deposits or payments.

Service Charges

Fees imposed by the bank for account maintenance or transactions, reducing the company's book balance.

Interest Revenue

Earnings credited by the bank to the company's account for holding funds, increasing the book balance.

NSF Checks

Customer checks deposited by the company that are returned unpaid due to insufficient funds in the payer's account.

Adjusted Balance

Final reconciled cash amount that matches both the bank statement and company records after all adjustments.

Internal Control

Procedures and policies, such as reconciliations, designed to safeguard assets and ensure accurate financial records.

Time Lag

Delay between recording transactions in company books and their appearance on the bank statement.

Cash

Most liquid asset, easily accessible and susceptible to theft, requiring strong controls like reconciliations.

BackBack

BackBack

04:57

04:57