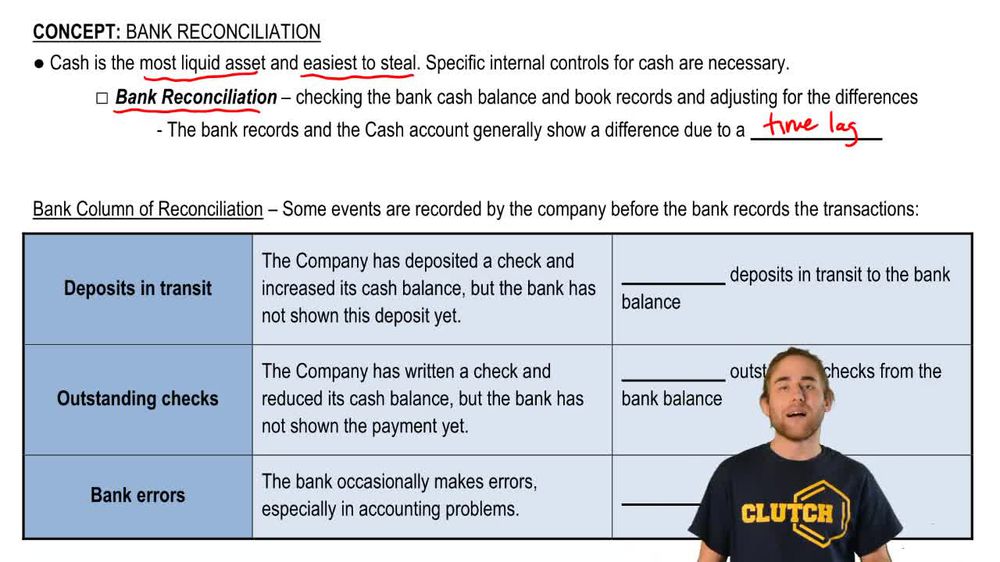

Bank reconciliations can reveal unauthorized transactions or discrepancies that may indicate fraud.

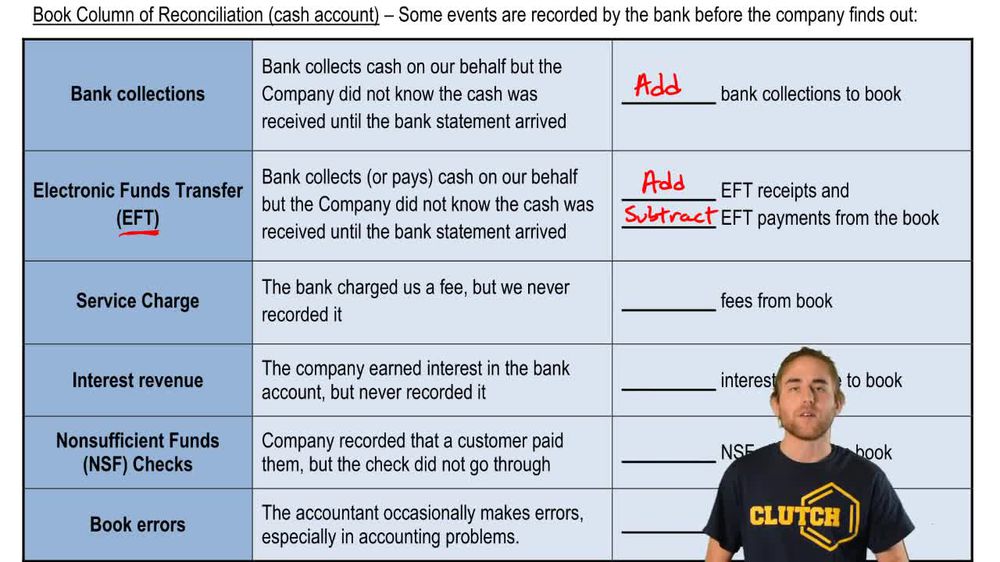

What is the impact of not recording a bank collection in the company's books?

The company's cash balance will be understated until the collection is recorded.

What is the impact of not recording a service charge in the company's books?

The company's cash balance will be overstated until the charge is recorded.

What is the impact of not recording an NSF check in the company's books?

The company's cash balance will be overstated until the NSF check is recorded.

What is the impact of not recording interest revenue in the company's books?

The company's cash balance will be understated until the interest is recorded.

What is the impact of not recording an EFT payment in the company's books?

The company's cash balance will be overstated until the payment is recorded.

What is the impact of not recording an EFT receipt in the company's books?

The company's cash balance will be understated until the receipt is recorded.

What is the impact of not correcting a book error during reconciliation?

The company's cash balance will remain inaccurate, leading to potential financial misstatements.

What is the impact of not correcting a bank error during reconciliation?

The bank balance will remain inaccurate, leading to discrepancies between the bank and company records.

Why is it important for the adjusted bank balance and adjusted book balance to be equal after reconciliation?

Equality ensures that all transactions and errors have been properly accounted for, confirming the accuracy of cash records.

What are the most common items found in a bank reconciliation?

The most common items are deposits in transit, outstanding checks, errors, service charges, interest revenue, and NSF checks.

How does a company record a correction for a bank error discovered during reconciliation?

The company contacts the bank to correct the error and adjusts the bank balance in the reconciliation.

How does a company record a correction for a book error discovered during reconciliation?

The company makes a journal entry to correct the error in its accounting records.

What is the role of timing differences in the bank reconciliation process?

Timing differences explain why some transactions appear in the company's records but not yet in the bank statement, or vice versa.

How does a company ensure all cash transactions are recorded accurately?

By performing regular bank reconciliations and making necessary adjusting entries.

What is the effect of failing to perform a bank reconciliation on a regular basis?

It increases the risk of undetected errors, fraud, and inaccurate financial statements.

What is a credit memorandum from the bank in the context of bank reconciliation?

A credit memorandum from the bank is a notification that the bank has increased the company's account balance, typically due to items such as bank collections or interest revenue. The company learns about these increases when reviewing the bank statement and must adjust its records accordingly.

For what types of transactions might a bank issue a credit memorandum?

A bank may issue a credit memorandum for transactions that increase the company's account balance, such as bank collections (when the bank collects money on behalf of the company) and interest revenue earned on the account.

How are credit memos from the bank treated during the bank reconciliation process?

During bank reconciliation, credit memos from the bank are added to the company's book balance because they represent increases in cash that the company was not aware of until receiving the bank statement.

Back

Back

04:57

04:57