Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Depreciation: Declining Balance definitions

You can tap to flip the card.

Double Declining Balance Method

You can tap to flip the card.

👆

Double Declining Balance Method

An accelerated approach allocating more depreciation to early years by applying twice the straight-line rate to the asset's book value.

Track progress

Control buttons has been changed to "navigation" mode.

1/14

Related flashcards

Related practice

Recommended videos

Depreciation: Declining Balance quiz #1

Depreciation: Declining Balance

10 Terms

Depreciation: Declining Balance

8. Long Lived Assets

10 problems

Topic

Depreciation: Units-of-Activity

8. Long Lived Assets

10 problems

Topic

8. Long Lived Assets - Part 1 of 2

14 topics

15 problems

Chapter

8. Long Lived Assets - Part 2 of 2

1 topic

3 problems

Chapter

Guided course

12:39

Double Declining Balance (DDB) Depreciation

1543

views

23

rank

1

comments

Guided course

07:25

Double Declining Balance (DDB) Depreciation

1903

views

28

rank

Terms in this set (14)

Hide definitions

Double Declining Balance Method

An accelerated approach allocating more depreciation to early years by applying twice the straight-line rate to the asset's book value.

Depreciation Expense

The annual allocation of an asset's cost, reducing net income and taxable income, especially higher in early years with accelerated methods.

Fixed Asset

A long-term tangible resource acquired for business use, expected to provide benefits over multiple years.

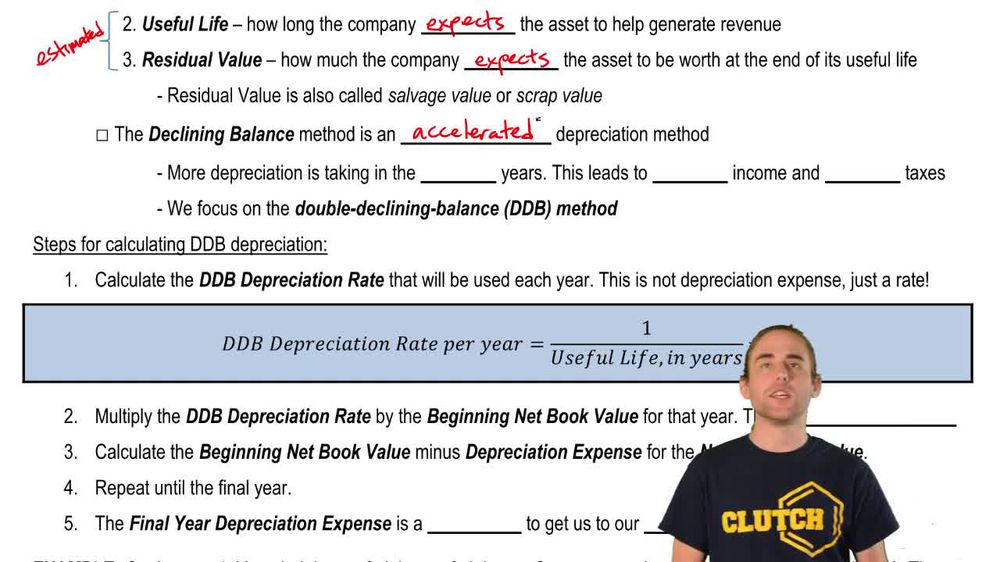

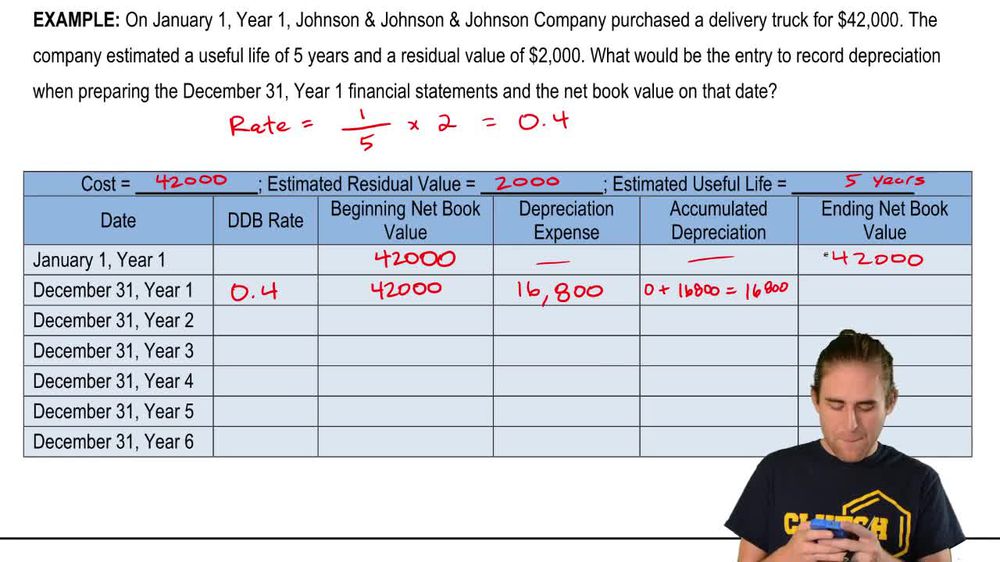

Useful Life

The estimated period an asset is expected to contribute to revenue generation for a company.

Residual Value

The anticipated worth of an asset at the end of its useful life, also known as salvage or scrap value.

Depreciation Rate

A percentage calculated as twice the reciprocal of useful life, used annually to determine depreciation under the double declining balance method.

Net Book Value

The asset's cost minus accumulated depreciation, serving as the base for annual depreciation calculations.

Accelerated Depreciation

A method that allocates higher depreciation expenses in the early years and lower amounts in later years of an asset's life.

Depreciable Base

The total amount of an asset's cost subject to depreciation over its useful life.

Plug

A final adjustment in the last year of depreciation to ensure the asset's book value matches its residual value.

Straight-Line Depreciation

A method allocating equal depreciation expense each year, subtracting residual value at the start.

Tax Benefit

A reduction in taxable income resulting from higher early-year depreciation expenses.

Salvage Value

An alternative term for residual value, representing expected asset worth after use.

Scrap Value

Another synonym for residual value, indicating the estimated end-of-life value of an asset.

BackBack

BackBack

12:39

12:39