Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

GAAP vs. IFRS: Adjusting Entries definitions

You can tap to flip the card.

GAAP

You can tap to flip the card.

👆

GAAP

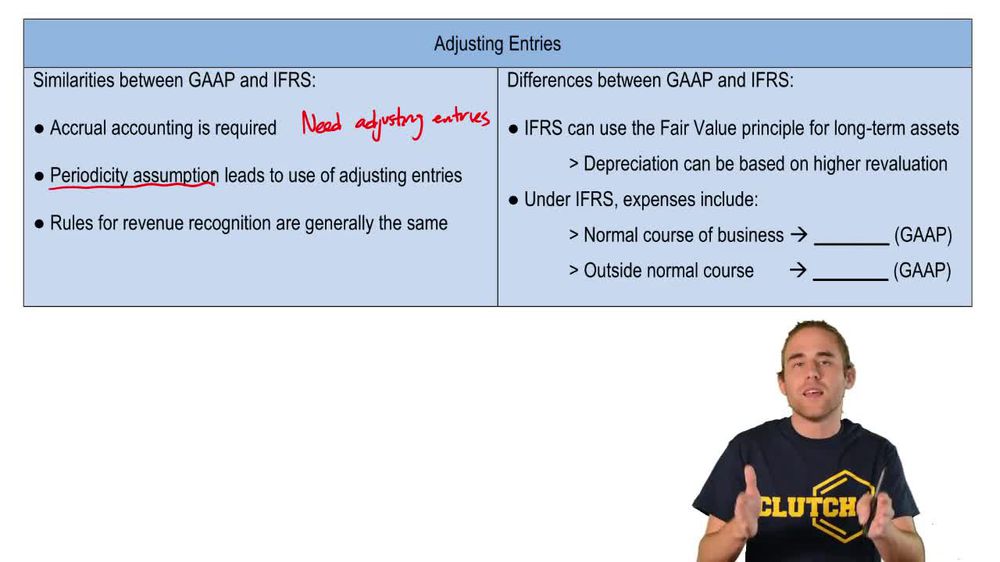

U.S. accounting framework established by FASB, emphasizing consistency and comparability in financial reporting.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Adjusting Entries quiz

GAAP vs. IFRS: Adjusting Entries

15 Terms

GAAP vs. IFRS: Adjusting Entries

15. GAAP vs IFRS

10 problems

Topic

GAAP vs. IFRS: Merchandising

15. GAAP vs IFRS

10 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

04:03

GAAP vs. IFRS: Adjusting Entries

350

views

10

rank

Terms in this set (15)

Hide definitions

GAAP

U.S. accounting framework established by FASB, emphasizing consistency and comparability in financial reporting.

IFRS

International accounting standards set by IASB, focusing on global comparability and often allowing asset revaluation.

FASB

U.S. organization responsible for developing and updating generally accepted accounting principles.

IASB

International body that creates and maintains standards for financial reporting used outside the U.S.

Accrual Accounting

Method requiring revenues and expenses to be recorded when earned or incurred, not when cash is exchanged.

Periodicity Assumption

Concept of dividing a business's ongoing activities into artificial time periods for reporting purposes.

Adjusting Entries

End-of-period journal entries ensuring revenues and expenses are recorded in the correct accounting period.

Revenue Recognition

Guideline dictating when and how income is formally recorded in the financial statements.

Fair Value Principle

IFRS guideline allowing assets to be reported at current market value, impacting asset valuation and depreciation.

Depreciation

Systematic allocation of the cost of a long-term asset over its useful life.

Revaluation

IFRS-permitted process of adjusting the book value of long-term assets to reflect current fair market value.

Expense

Outflow or using up of assets in the normal course of business operations.

Loss

Financial decrease from events outside normal business activities, such as selling investments below cost.

Long-term Asset

Resource expected to provide economic benefit to a business for more than one year, subject to depreciation.

Balance Sheet

Financial statement presenting a company's assets, liabilities, and equity at a specific point in time.

BackBack

BackBack

04:03

04:03