Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

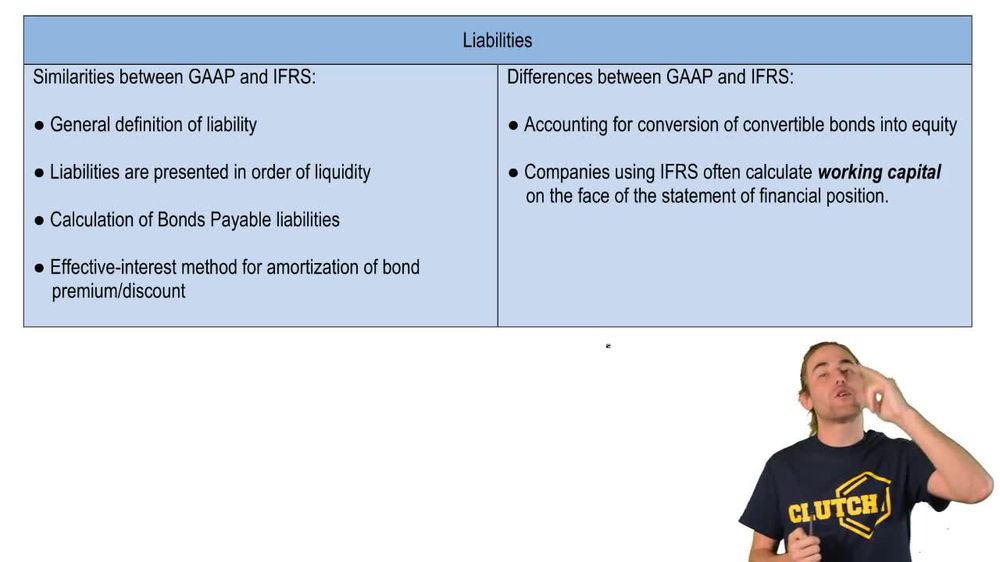

GAAP vs. IFRS: Liabilities definitions

You can tap to flip the card.

GAAP

You can tap to flip the card.

👆

GAAP

U.S. accounting framework established by the Financial Accounting Standards Board, guiding financial reporting and liability presentation.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Liabilities quiz

GAAP vs. IFRS: Liabilities

15 Terms

GAAP vs. IFRS: Liabilities

15. GAAP vs IFRS

9 problems

Topic

GAAP vs. IFRS: Stockholders' Equity

15. GAAP vs IFRS

10 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

03:02

GAAP vs. IFRS: Liabilities

358

views

2

rank

Terms in this set (15)

Hide definitions

GAAP

U.S. accounting framework established by the Financial Accounting Standards Board, guiding financial reporting and liability presentation.

IFRS

International accounting standards set by the International Accounting Standards Board, used globally for financial reporting.

Liability

Obligation representing a future outflow of resources, typically listed by liquidity on financial statements.

Financial Accounting Standards Board

U.S. organization responsible for developing and issuing generally accepted accounting principles.

International Accounting Standards Board

Global body that creates and maintains international financial reporting standards.

Bonds Payable

Long-term debt instruments requiring periodic interest payments and eventual repayment of principal.

Effective Interest Method

Technique for amortizing bond premiums or discounts, ensuring interest expense reflects carrying value over time.

Convertible Bonds

Debt securities that can be exchanged for shares of stock, initially recorded as liabilities.

Equity

Ownership interest in a company, often resulting from conversion of certain debt instruments like convertible bonds.

Working Capital

Difference between current assets and current liabilities, indicating short-term financial health.

Statement of Financial Position

IFRS term for the balance sheet, displaying assets, liabilities, and equity at a specific point in time.

Balance Sheet

Financial statement showing a company's assets, liabilities, and equity, known as the statement of financial position under IFRS.

Liquidity

Order in which assets or liabilities are presented, based on how quickly they can be converted to cash or settled.

Current Assets

Resources expected to be converted to cash or used up within one year, crucial for working capital calculation.

Current Liabilities

Obligations due within one year, subtracted from current assets to determine working capital.

BackBack

BackBack

03:02

03:02