System where revenues and expenses are recorded when earned or incurred, not when cash is exchanged, ensuring financial statements reflect true activity.

Adjusting Journal Entry

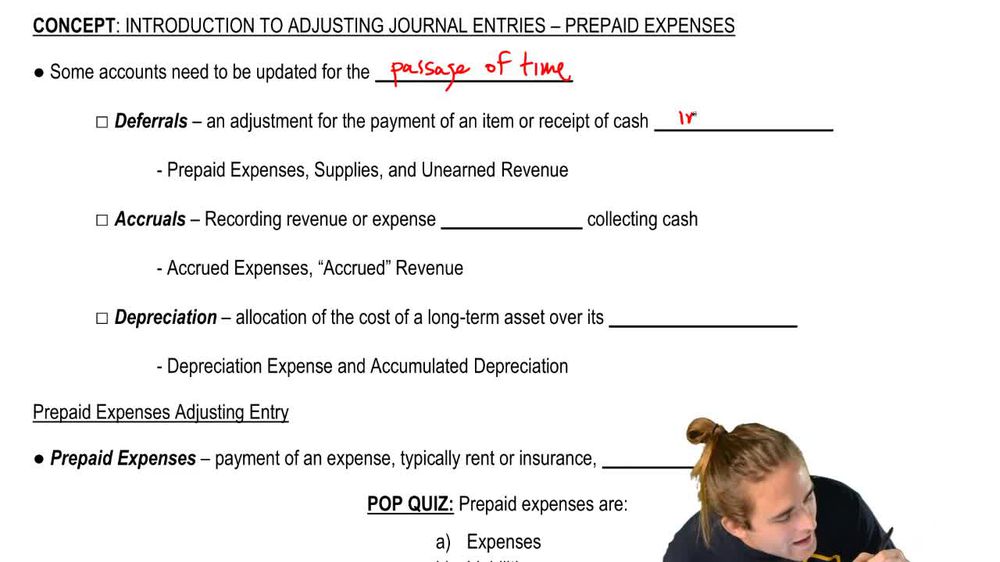

Update made at period end to ensure account balances reflect the passage of time and match revenues and expenses to the correct period.

Deferral

Situation where cash is exchanged before the related revenue is earned or expense is incurred, requiring later adjustment.

Accrual

Situation where revenue or expense is recognized before cash is exchanged, reflecting activity that has occurred but not yet settled in cash.

Depreciation

Allocation of the cost of a long-term asset over its useful life, spreading expense gradually rather than all at once.

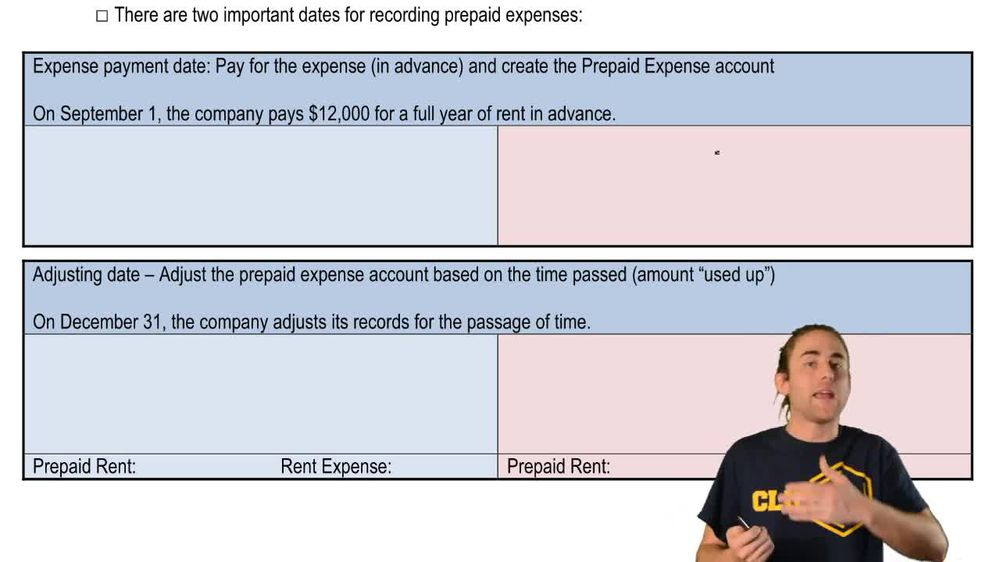

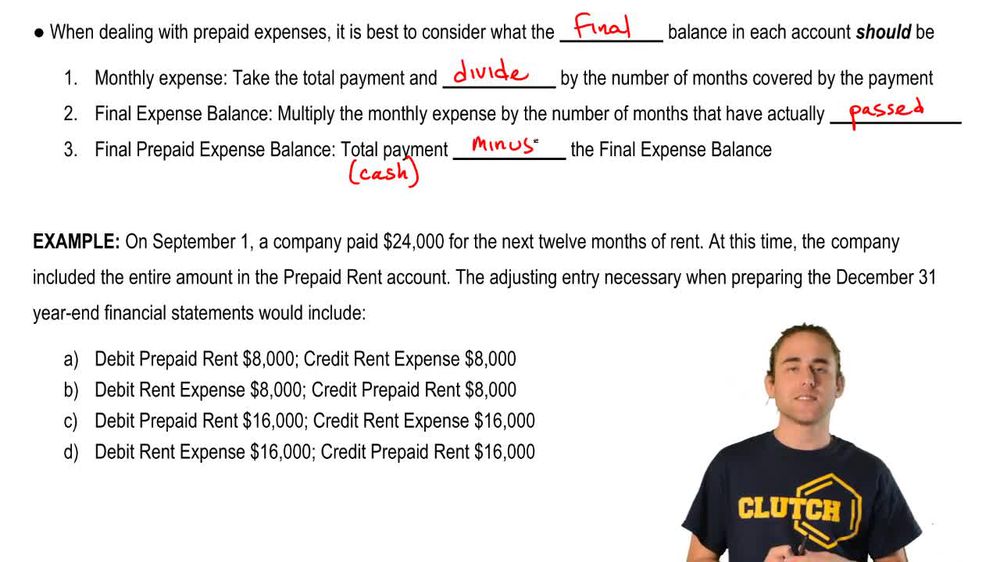

Prepaid Expense

Asset representing payment made in advance for goods or services to be received in the future, such as rent or insurance.

Prepaid Rent

Asset account holding the value of rent paid in advance, reduced over time as the rented space is used.

Rent Expense

Account reflecting the portion of prepaid rent that has been used up during a specific period.

Cash Basis Accounting

Method where revenues and expenses are recorded only when cash is received or paid, regardless of when activity occurs.

Accrual Basis Accounting

Method where revenues and expenses are recorded when earned or incurred, matching them to the period in which they happen.

Asset

Resource with future economic benefit, such as prepaid expenses, that is owned or controlled by a business.

Journal Entry

Record in the accounting system documenting a financial transaction, showing accounts affected and amounts debited or credited.

Credit

Entry on the right side of an account, typically decreasing assets or increasing liabilities and equity.

Debit

Entry on the left side of an account, typically increasing assets or expenses and decreasing liabilities or equity.

Balance Sheet

Financial statement showing a company's assets, liabilities, and equity at a specific point in time.

Back

Back

04:19

04:19