Why is it incorrect to record the entire prepaid expense as an expense immediately under accrual accounting?

Because the benefit of the expense extends over multiple periods, and only the portion used should be expensed each period.

What is the impact on net income if prepaid expenses are not adjusted at period-end?

Net income will be overstated because expenses are understated.

How does the adjusting entry for prepaid expenses demonstrate the matching principle?

It ensures expenses are recognized in the same period as the related benefits are received.

What is the correct adjusting entry if a company has \$5,000 in prepaid insurance and one month (\$1,000) has expired?

Debit insurance expense \$1,000 and credit prepaid insurance \$1,000.

If a company paid \$36,000 for a 12-month lease and 6 months have passed, what is the adjusting entry?

Debit rent expense \$18,000 and credit prepaid rent \$18,000.

What is the effect of an adjusting entry for prepaid expenses on the asset and expense accounts?

The asset account decreases and the expense account increases by the amount used.

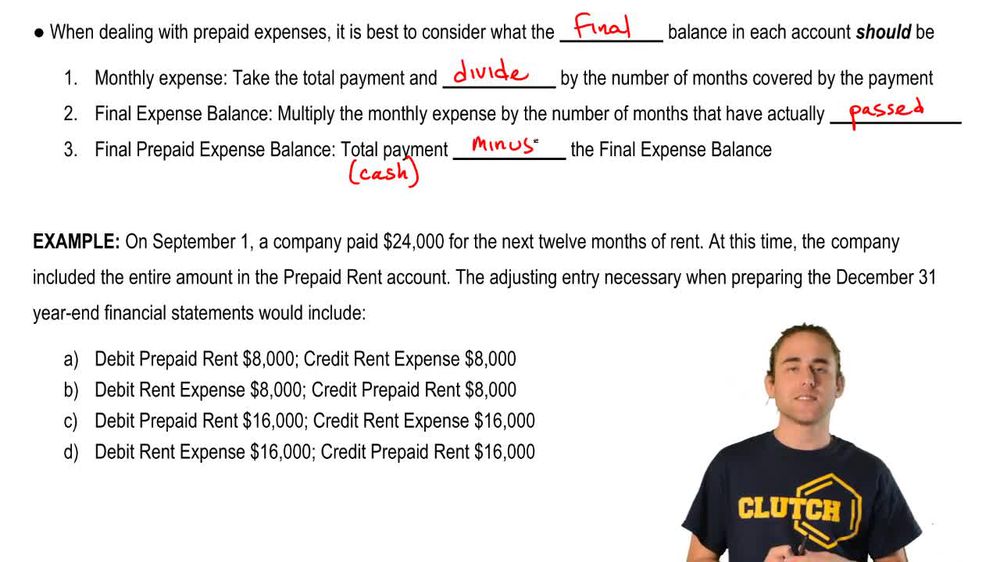

How do you determine the correct balance in a prepaid expense account at period-end?

Subtract the total expense recognized from the original prepaid amount to find the remaining asset balance.

What is the adjusting entry if a company paid \$8,000 for 8 months of insurance and 3 months have passed?

Debit insurance expense \$3,000 and credit prepaid insurance \$3,000.

Why is it important to consider the number of months elapsed when adjusting prepaid expenses?

To ensure only the portion of the expense that has been used is recognized in the current period.

What is the correct adjusting entry if a company paid \$10,800 for a 12-month insurance policy and 5 months have passed?

Debit insurance expense \$4,500 and credit prepaid insurance \$4,500.

How does the adjusting entry for prepaid expenses affect the company's financial position?

It provides a more accurate representation of assets and expenses, improving the reliability of financial statements.

What is the main objective of adjusting entries for prepaid expenses at the end of the period?

To match expenses with the periods in which the related benefits are received, ensuring accurate financial reporting.

In which section of the balance sheet do prepaid expenses appear?

Prepaid expenses appear in the assets section of the balance sheet.

How is prepaid insurance reported on the balance sheet?

Prepaid insurance is reported as an asset on the balance sheet.

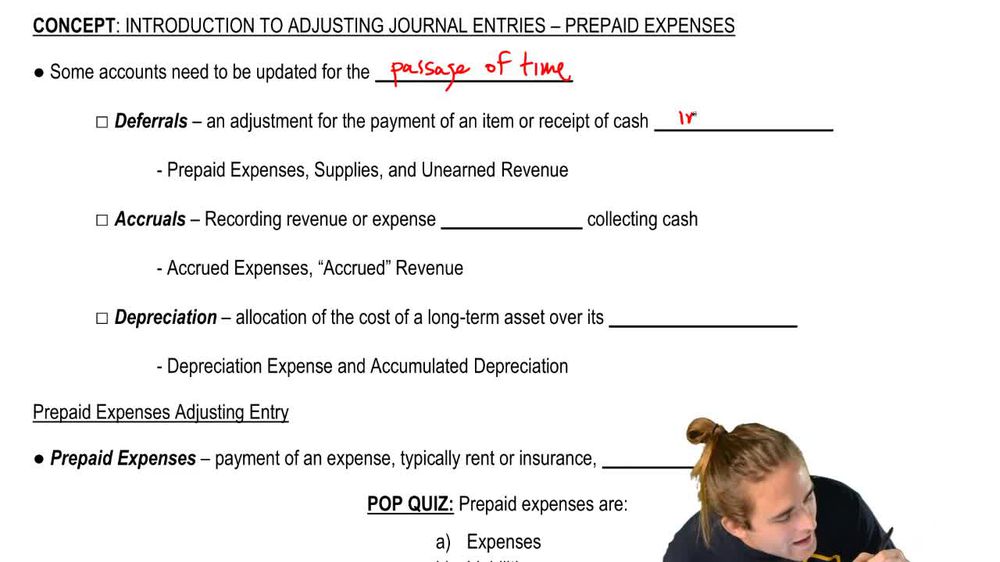

Why are prepaid expenses considered assets in financial accounting?

Prepaid expenses are considered assets because they represent future economic benefits that the company will receive, such as rent or insurance paid in advance.

What type of asset is insurance on inventory classified as when paid in advance?

Insurance on inventory paid in advance is classified as a prepaid expense, which is an asset.

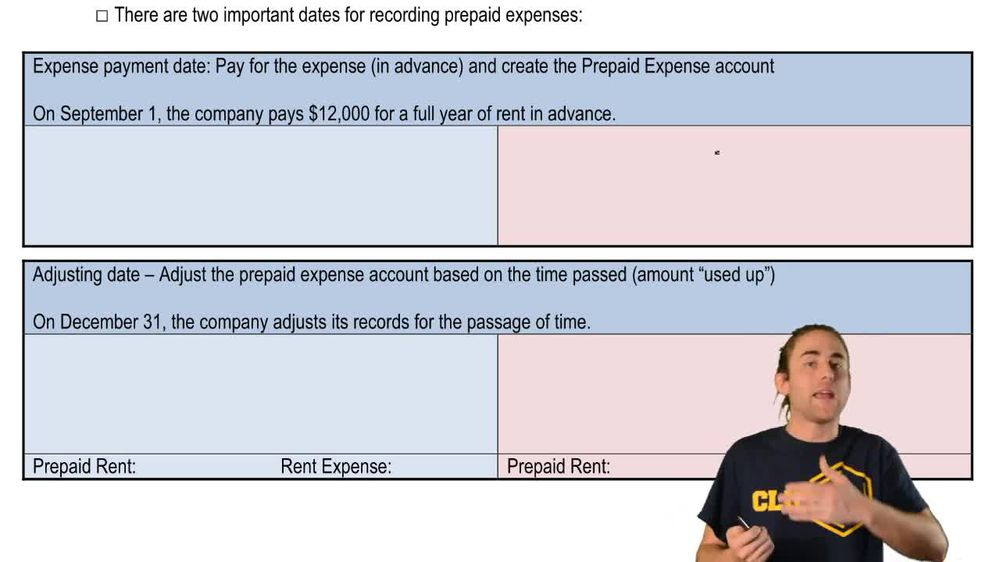

What is the initial journal entry for a prepaid expense such as rent or insurance?

The initial journal entry for a prepaid expense is to debit the prepaid expense account and credit cash for the amount paid.

How is the adjusting entry for a prepaid expense recorded at the end of an accounting period?

The adjusting entry for a prepaid expense is to debit the related expense account (e.g., rent expense) and credit the prepaid expense account to reflect the amount used during the period.

What is the process for determining the amount to adjust for a prepaid expense at period end?

To adjust for a prepaid expense at period end, calculate the monthly expense by dividing the total prepaid amount by the number of months covered, multiply by the number of months elapsed, and record an adjusting entry for the amount used.

Back

Back

04:19

04:19