Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Summary of Adjusting Entries definitions

You can tap to flip the card.

Accrual Accounting

You can tap to flip the card.

👆

Accrual Accounting

System where revenues and expenses are recognized when earned or incurred, not when cash is exchanged.

Track progress

Control buttons has been changed to "navigation" mode.

1/14

Related flashcards

Related practice

Recommended videos

Summary of Adjusting Entries quiz #1

Summary of Adjusting Entries

11 Terms

Summary of Adjusting Entries

3. Accrual Accounting Concepts

10 problems

Topic

Unadjusted vs Adjusted Trial Balance

3. Accrual Accounting Concepts

10 problems

Topic

3. Accrual Accounting Concepts

12 topics

14 problems

Chapter

Guided course

07:45

Summary of Adjusting Entries

2412

views

73

rank

1

comments

Terms in this set (14)

Hide definitions

Accrual Accounting

System where revenues and expenses are recognized when earned or incurred, not when cash is exchanged.

Prepaid Expenses

Payments made in advance for goods or services, recorded as assets until consumed or expired.

Rent Expense

Cost recognized over time for using property or space, often adjusted from prepaid amounts.

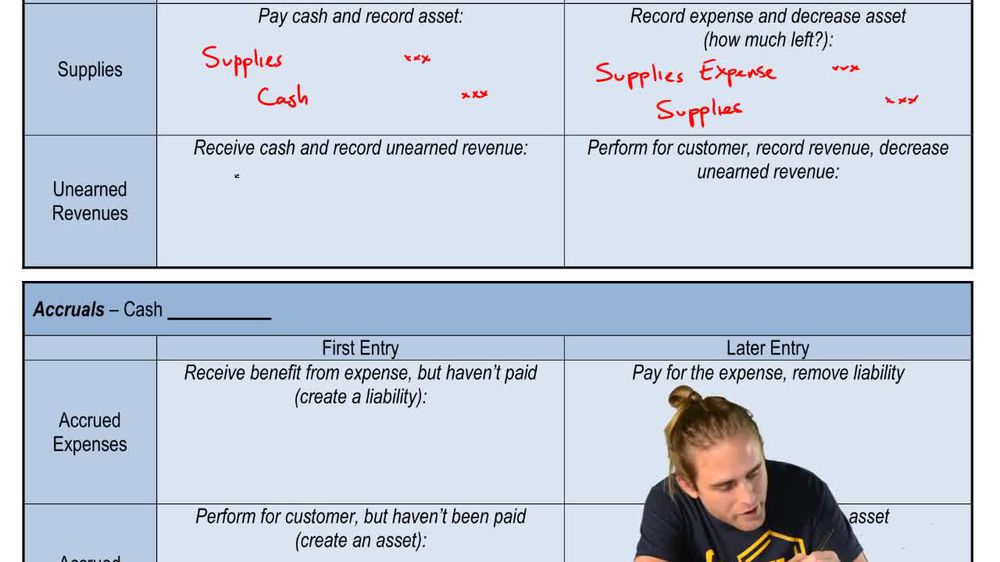

Supplies

Assets purchased for future use in operations, later expensed as they are consumed.

Supplies Expense

Amount representing the cost of supplies used during a period, calculated by subtracting ending supplies from beginning balance.

Unearned Revenue

Liability created when cash is received before goods or services are delivered to customers.

Revenue

Income earned from providing goods or services, recognized when performance obligations are satisfied.

Accrued Expenses

Obligations for expenses incurred but not yet paid, recorded as liabilities until settled.

Accrued Liability

Balance sheet account representing amounts owed for expenses recognized but unpaid at period end.

Accounts Receivable

Asset representing amounts owed by customers for goods or services delivered but not yet paid for.

Depreciation

Systematic allocation of the cost of a long-term asset over its useful life to expense.

Depreciation Expense

Portion of an asset's cost recognized as expense in each period to reflect usage or wear.

Accumulated Depreciation

Contra asset account showing total depreciation taken on an asset, reducing its book value.

Net Book Value

Amount calculated by subtracting accumulated depreciation from an asset's original cost.

BackBack

BackBack

07:45

07:45