Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Depreciation: Units-of-Activity definitions

You can tap to flip the card.

Depreciation

You can tap to flip the card.

👆

Depreciation

Allocation of an asset's cost over its useful life to match expense with revenue generated by the asset.

Track progress

Control buttons has been changed to "navigation" mode.

1/13

Related flashcards

Related practice

Recommended videos

Depreciation: Units-of-Activity quiz

Depreciation: Units-of-Activity

15 Terms

Depreciation: Units-of-Activity

8. Long Lived Assets

10 problems

Topic

Depreciation: Summary of Main Methods

8. Long Lived Assets

10 problems

Topic

8. Long Lived Assets - Part 1 of 2

14 topics

15 problems

Chapter

8. Long Lived Assets - Part 2 of 2

1 topic

3 problems

Chapter

Guided course

04:54

Units-of-Activity Depreciation

1013

views

21

rank

Guided course

07:44

Units-of-Activity Depreciation

895

views

10

rank

1

comments

Guided course

03:17

Units-of-Activity Depreciation

1212

views

21

rank

Terms in this set (13)

Hide definitions

Depreciation

Allocation of an asset's cost over its useful life to match expense with revenue generated by the asset.

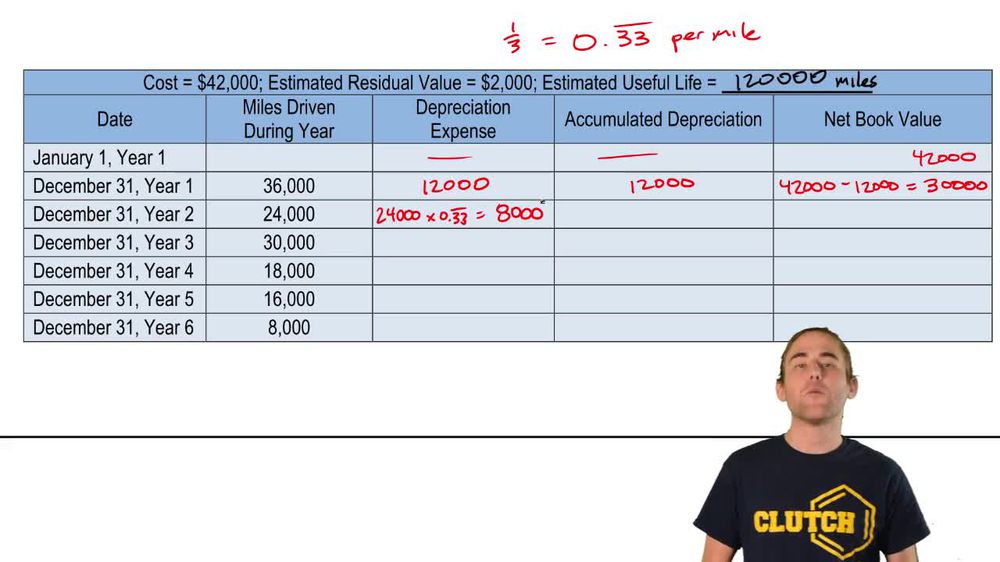

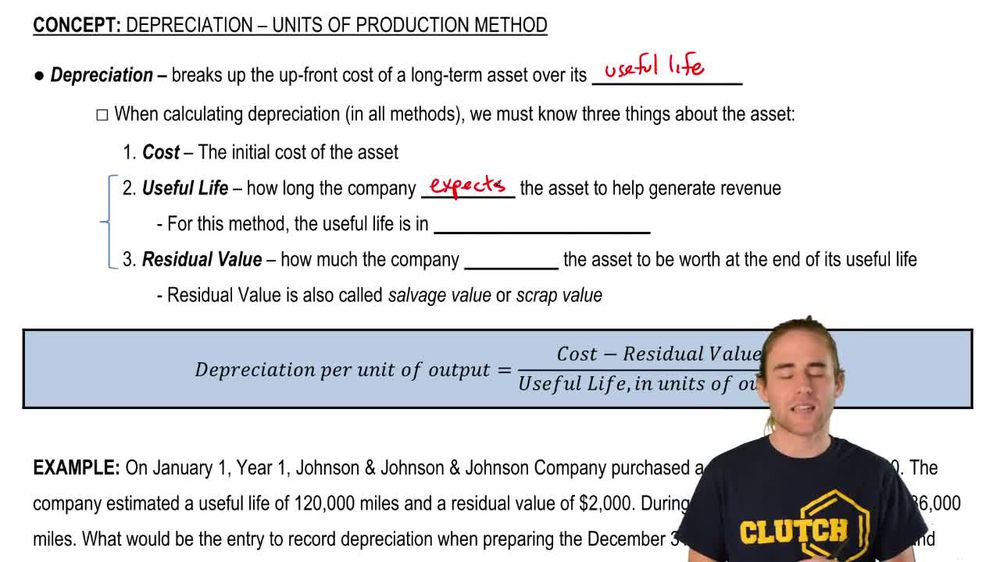

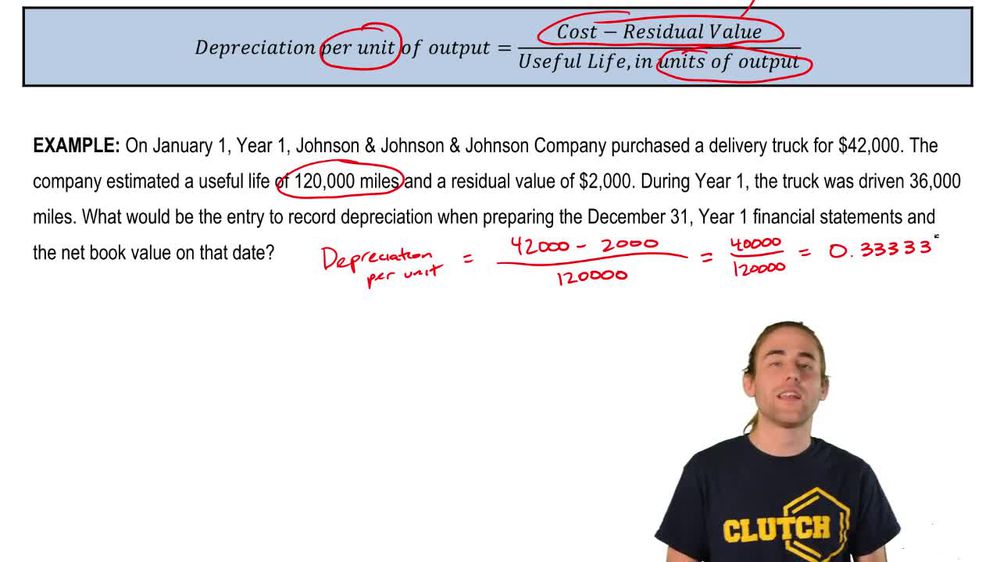

Units of Production Method

Depreciation approach based on asset usage, such as miles driven or units produced, rather than passage of time.

Units of Activity Method

Alternative name for the units of production method, focusing on output or activity level for depreciation.

Fixed Asset

Long-term tangible resource, like equipment or vehicles, used in operations and subject to depreciation.

Useful Life

Estimated total output or period an asset is expected to contribute to revenue generation.

Residual Value

Expected worth of an asset at the end of its useful life, also called salvage or scrap value.

Salvage Value

Alternative term for residual value, representing anticipated value after asset's productive use.

Scrap Value

Another synonym for residual value, indicating estimated disposal value after use.

Depreciable Base

Difference between asset's initial cost and its residual value, representing total amount to be depreciated.

Depreciation Per Unit

Amount of depreciation assigned to each unit of output or activity, calculated using the method's formula.

Initial Cost

Original purchase price or investment made to acquire a fixed asset.

Estimated Units of Production

Predicted total output, such as miles or units, an asset will provide over its useful life.

Output

Measure of production or activity, such as units produced or miles driven, used to allocate depreciation.

BackBack

BackBack

04:54

04:54