Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Classical Model and Keynesian Model definitions

You can tap to flip the card.

Classical Model

You can tap to flip the card.

👆

Classical Model

An economic framework assuming flexible prices and wages, full employment, and self-correction without government action.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Classical Model and Keynesian Model quiz

Classical Model and Keynesian Model

15 Terms

Classical Model and Keynesian Model

22. Macroeconomic Schools of Thought

10 problems

Topic

Monetarist Model

22. Macroeconomic Schools of Thought

10 problems

Topic

24. Macroeconomic Schools of Thought

7 topics

15 problems

Chapter

Guided course

02:54

Classical Model

1643

views

29

rank

Guided course

03:41

Graphical Comparison of Classical Model and Keynesian Model

1539

views

28

rank

Guided course

03:04

Keynesian Model

1559

views

21

rank

Terms in this set (15)

Hide definitions

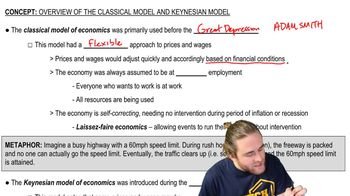

Classical Model

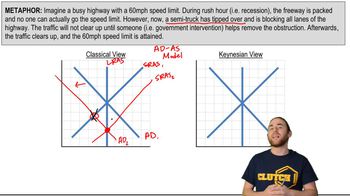

An economic framework assuming flexible prices and wages, full employment, and self-correction without government action.

Keynesian Model

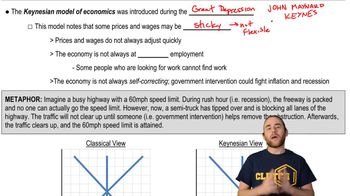

An economic framework emphasizing sticky prices and wages, possible unemployment, and the need for government intervention.

Flexible Prices

A condition where costs of goods and services adjust rapidly to changes in market conditions, restoring equilibrium quickly.

Sticky Wages

A situation where compensation does not adjust quickly to economic shifts, often due to contracts or institutional factors.

Full Employment

A state where all available labor resources are being used efficiently, with anyone seeking work able to find a job.

Self-Correction

A process where market forces alone restore economic stability after disruptions, without outside intervention.

Laissez Faire

An approach advocating minimal government involvement in economic affairs, allowing markets to operate freely.

Government Intervention

Actions by public authorities to influence economic outcomes, especially during recessions or inflation.

Aggregate Demand

The total demand for goods and services within an economy at a given overall price level and time period.

Aggregate Supply

The total output of goods and services that firms in an economy are willing to produce at a given price level.

Short Run Equilibrium

A temporary state where aggregate demand and aggregate supply intersect, possibly away from full employment.

Long Run Equilibrium

A condition where the economy's output matches its potential, with no pressure for prices or output to change.

Potential GDP

The highest level of output an economy can sustain over time without increasing inflation.

Invisible Hand

A metaphor for the self-regulating nature of markets, where individual actions collectively benefit the economy.

Recession

A period of declining economic activity, often marked by reduced output and rising unemployment.

BackBack

BackBack

02:54

02:54