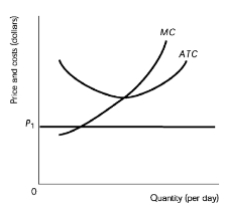

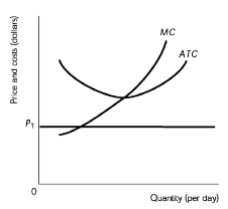

In a perfectly competitive market, the long-run equilibrium is characterized by firms producing at the minimum average total cost (ATC), where price equals ATC, resulting in zero economic profit. This equilibrium is stable, meaning that even with fluctuations in demand, the market will adjust back to this point over time.

When there is an increase in demand, the demand curve shifts to the right, leading to a higher equilibrium price and quantity in the short run. This increase in price allows firms to earn economic profits, as the price exceeds the average total cost. In response to these profits, new firms are incentivized to enter the market, increasing the overall supply.

As more firms enter, the supply curve shifts to the right, which eventually drives the price back down to the original equilibrium price (P1). This process continues until the market reaches a new equilibrium where the price once again equals the minimum ATC, eliminating the economic profits. The result is a larger quantity supplied in the market, but the individual firms return to producing at the minimum ATC, ensuring that no economic profits are made in the long run.

This dynamic illustrates the self-correcting nature of competitive markets, where shifts in demand lead to temporary profits or losses, but ultimately stabilize at the long-run equilibrium defined by the minimum average total cost. Thus, regardless of demand fluctuations, the market consistently returns to a state where price equals minimum ATC, ensuring efficiency and sustainability in the long run.